The 2020 edition of The Tatra Summit Insight Report marks the birth of the CEE Strategic Transformation Index (STI), a new composite measure of economic progress for the region of Central and Eastern Europe (CEE). As the past decade concluded, 2020 began abruptly with an unprecedented and violent shock to the global economy caused by the COVID-19 pandemic. This placed the global economy into a standstill sending seismic shockwaves across our economies and societies, making it evident that its effects will long outlive the virus’ onset.

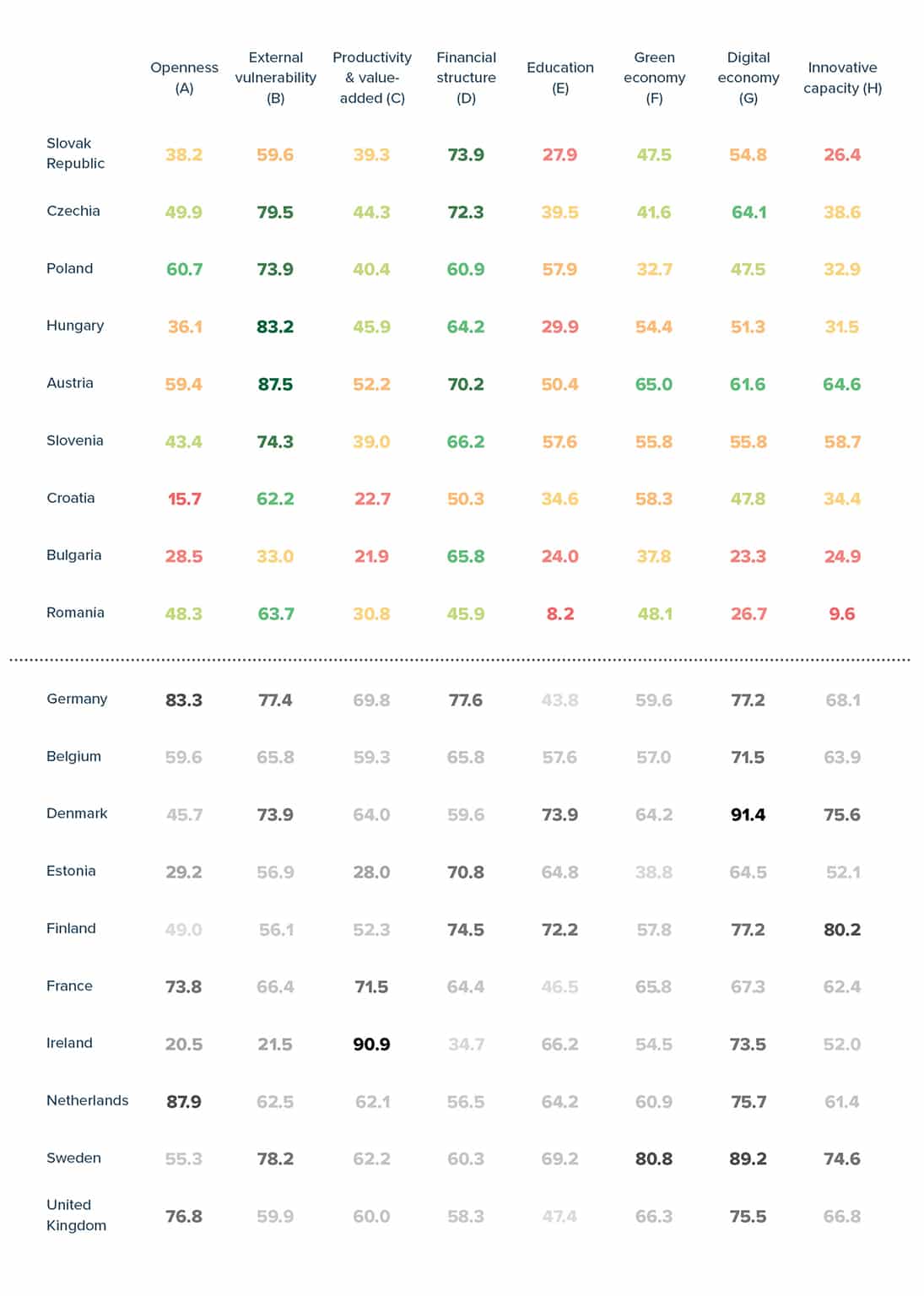

The STI caters to the plea of deep restructuring of the CEE economy, as it offers insights into the past multi-faceted economic performance of nine CEE economies while emphasizing key forward-looking policy areas to unlock sustainable long-term growth, including innovation, education, and the twin green and digital transition. As such, it provides a composite quantitative diagnostic tool for capturing economic progress in the region, by benchmarking the CEE region at an aggregate level and the nine CEE economies – Austria, Bulgaria, Croatia, Czechia, Hungary, Poland, Romania, the Slovak Republic, and Slovenia – individually, within a broader context of a selected control group of advanced European economies.

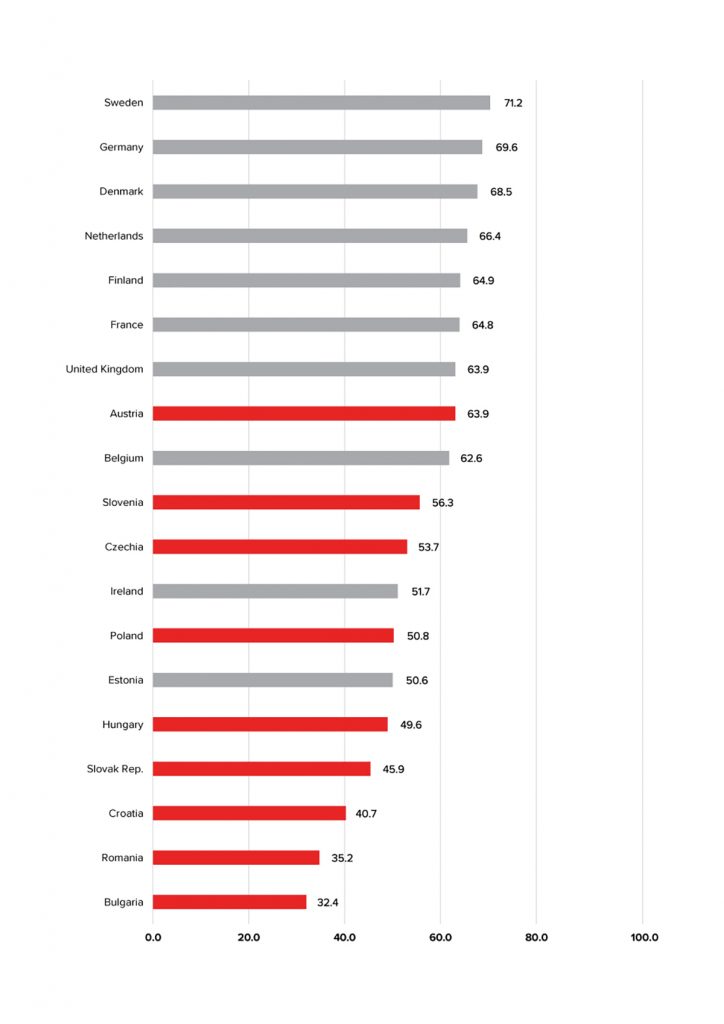

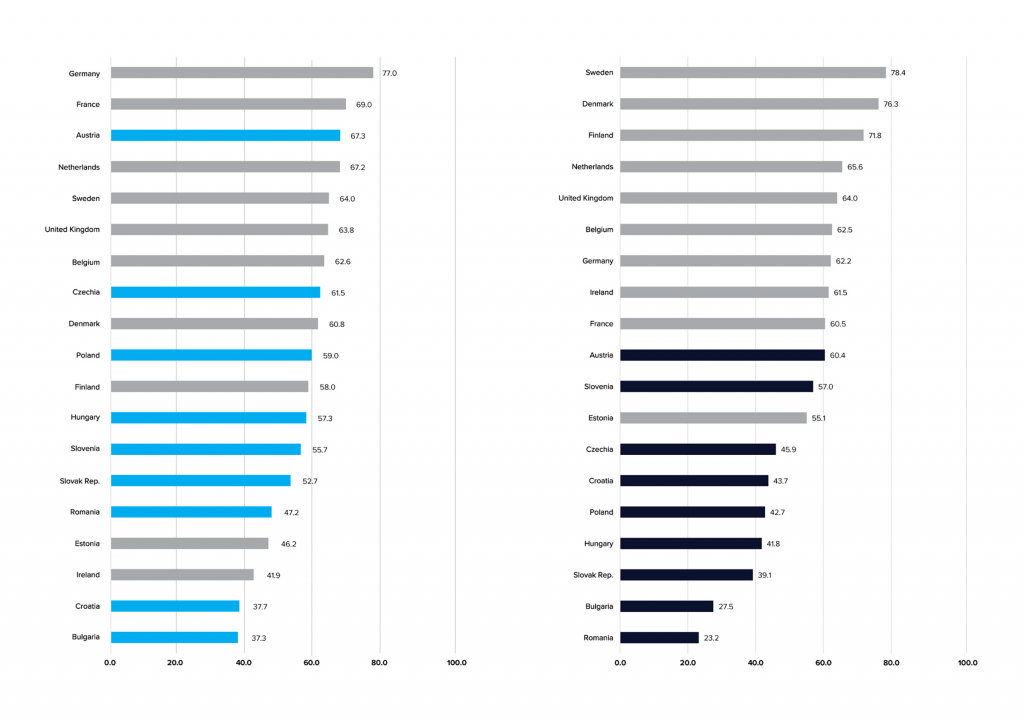

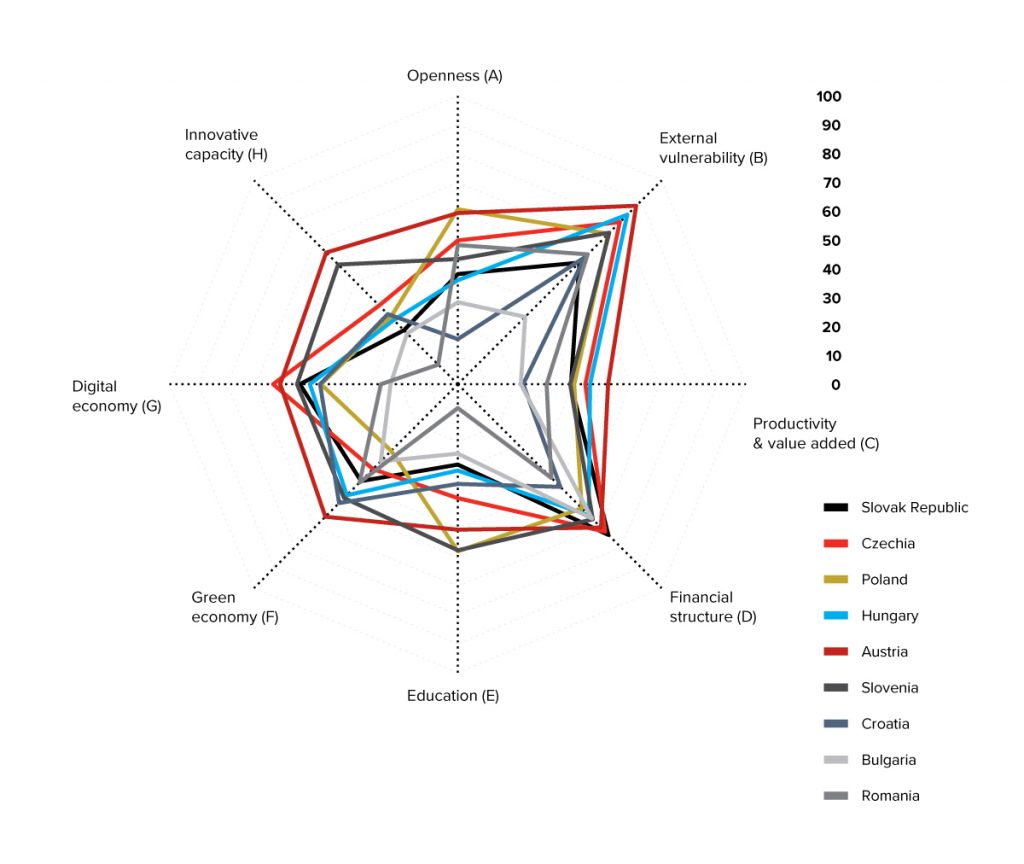

STI benchmarks a country’s ability, and that of the region, towards the strategic transformation frontier. It measures the extent to which the underlying macroeconomic, resilience and innovation drivers – both old and new – are in place, benchmarks relative progress of countries in terms of these drivers and presents the country strengths and weaknesses. Covering 9 CEE economies and 47 indicators in this first edition, the index identifies the best-performers in the CEE9 region when it comes to openness, external resilience, productivity and value-added, and financial structure; as well as innovation cluster of variables, including education, green and digital transition and innovative capacity.

The index is to be periodically updated before each Tatra Summit to provide a well-timed basis for policy dialogue on this platform. Availability at an aggregate regional-level and individual country-level offer insights into overall year-on-year regional and country performance, respectively. Eight disaggregated thematic clusters (i.e. sub-indices) offer more granular insights into macro-resilience and innovation developments and enable the identification of country strengths and weaknesses and the formulation of corresponding policy leads.

STI is being launched as a flagship initiative at the GLOBSEC Tatra Summit 2020. GLOBSEC Tatra Summit is an annual high-level gathering of political elites, top-of-the-line policy experts and researchers, private sector leaders, academia and third sector frontrunners which every October take the pulse of the European and by gathering over most pressing challenges and conundrums our economies and societies are facing. The GLOBSEC Tatra Summit platform thus serves to anchor the STI project and amplify its impacts. STI can be used as an evidence-basis to underpin the high-level policy dialogues taking place at the Tatra Summit platform by identifying key weakness areas, and as such, it is designed to suit policymakers and leaders in the quest of taking an informed action on a revived economic transformation policy dossier with a useful diagnostic tool. It can also help businesses in formulating their business strategies and establishing practices, buttressing economic transformation outcomes from the bottom-up. The bottom line is that the broad policy priority leads STI articulates are to offer a compass for strategic policy and business action in the CEE9 region on the path towards more dynamic, resilient and sustainable economies.